Chapter 2

Normative analysis

Edge worth box and general equilibrium

There are two types of equilibrium models used in an economy. They are Partial

Equilibrium & General Equilibrium.

Partial Equilibrium

Partial equilibrium is just the technical terms for demand and supply analysis. Partial equilibrium models consider only one market at a time, ignoring potential interactions across markets.

What is Partial Equilibrium?

Partial equilibrium is based on only a restricted range of data.

The effects of policy actions are examined only in the markets that are directly affected (apples not oranges)

Supply and demand curves are used to depict the price effects of policies.

Producer and consumer surplus is used to measure the welfare effects on participants in the market.

Ignores spillover effects on other industries/countries General Assumptions:

Country is relatively small • Sector in question is small

• No adjustment – short term

• Consumer preferences are fixed

• Perfect mobility of factors of production

No long term effects such as growth or reallocation of production factors are taken into account.

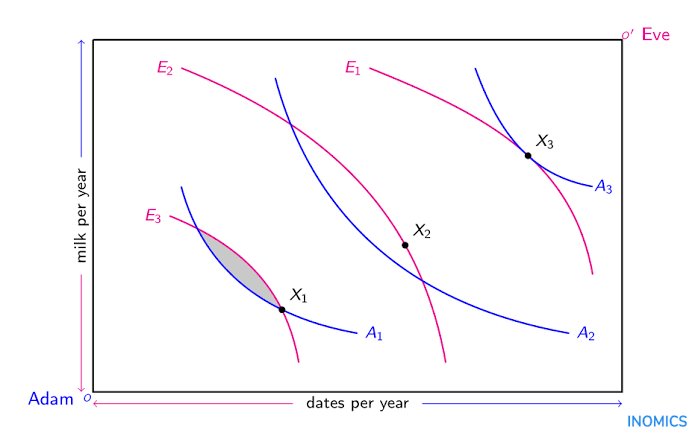

Edge worth box

In economics, an Edgeworth box, sometimes referred to as an Edgeworth-Bowley box, is a graphical representation of a market with just two commodities, X and Y, and two consumers.

Consider the following example of an economy with two individuals, Adam and Eve, and two items, dates and milk. The total number of dates in the economy is represented by the horizontal length of the box; the total amount of milk is measured by its vertical length.

What Is General Equilibrium?

In economics, general equilibrium exists when demand and supply are in perfect balance or harmony. The primary objective of this theory is to identify the exact circumstances under which demand and supply become equal to each other and prices become stable.

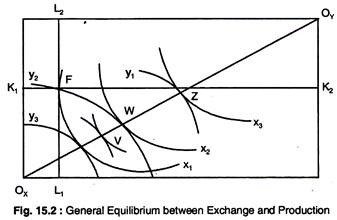

General equilibrium in exchange occurs when both individuals have the same MRS, which is a point on the contract curve. When the MRS = the MRT, there is a general equilibrium between exchange and production.

Pareto Optimality or Efficiency

Pareto efficiency or Pareto optimality is a situation where no action or allocation is available that makes one individual better off without making another worse off.

PARETO OPTIMALITY

Pareto Criterion

• Purpose

■ Pareto criterion is a technique for comparing or ranking alternative states of the economy

Definition of Pareto Criterion

▪ If it is possible to make at least one person better off in moving from state A to state B without making anyone else worse off, state B is ranked higher by society than state B.

There marginal conditions are as follows :

1) Efficiency in Exchange (Efficiency of distribution of commodities among

consumers)

2) Efficiency of Production (Efficiency of allocation of factors of production among

firms)

3) Efficiency in Product Mix or Composition of Output (Efficiency in allocation of

factors among commodities)

1)Efficiency of Exchange

The marginal rate of substitution between any two products must be the same for every individual who consumes both.

2)Efficiency of Production

No further improvements to society’s well being can be made through a reallocation of resources that makes at least one person better off without making someone else worse off.

3)Efficiency of Product / Output Mix

In a Pareto optimum state when no economic changes can make one individual better off without making at least one other individual worse off

These marginal conditions are based on the following assumptions :

a) Each individual has his own consumer preference and have definite amount of goods.

b) State of technology remains constant for production

c) Goods are perfectly divisible

d) All factors of production are perfectly mobile

e) Every individual wants to maximize his satisfaction.

f) Every individual purchases some quantities of all goods.

g) Producer tries to achieve least cost combination of factors.

First Fundamental Theorem

First Fundamental Theorem of Welfare Economics: The competitive equilibrium where supply equals demand, maximizes social efficiency.

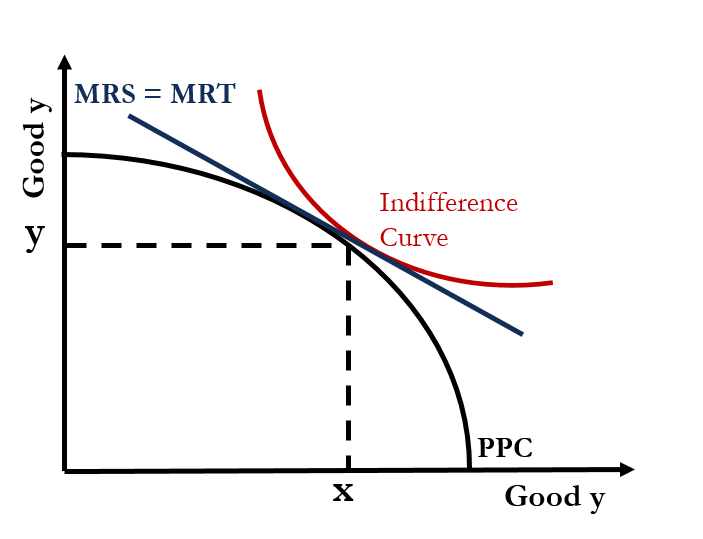

Mathematically, First Fundamental shows : MRSxy of A = MRSxy of B = MRTxy.

This theorem is based upon two important assumption :

a) Economy is in perfect competition.

b) A market exist for each and every commodity.

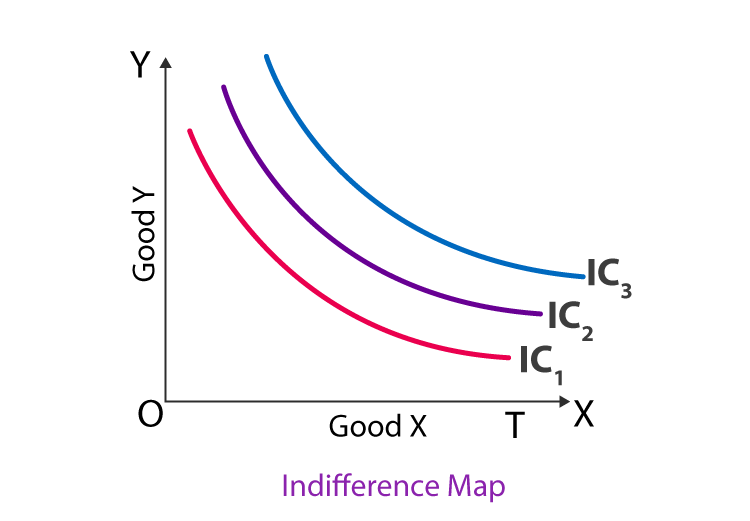

The Consumer Side

Each consumer maximizes his satisfaction and is in equilibrium at the point where the given

budget line is tangent to his indifference curve. In other words, each consumer is in

equilibrium when :

MRSxy of A =

𝑷𝒙/𝑷𝒚

—————– (1)

MRSxy of B =

𝑷𝒙/𝑷𝒚 —————– (2)

Thus, MRSxy of A = MRSxy of B is one of the necessary condition for pareto efficiency.

The Producer Side

Under the perfect competition, each firm to be in equilibrium produces so much output that

its marginal cost is equal to the price of the commodity.

Thus, for the firms in perfect competition, MCx = Px and Mcy = Py

Where MCx and MCy are marginal cost of Good X and Good Y respectively and Px and Py

are prices of Good X and Good Y.

Ratio of MCx to MCy shows the Ratio of Px to Py

𝑴𝑪𝒙/𝑴𝑪𝒚 = 𝑷𝒙/𝑷𝒚

The ratio of marginal costs of two commodities represents the marginal rate of

transformation between them. Therefore, for firms producing in perfect competition :

MRTxy = 𝑴𝑪𝒙/𝑴𝑪𝒚 = 𝑷𝒙/𝑷𝒚 ——————- (3)

The Equality

Since, under perfect competition, the ratio of prices of two commodities (Px/Py) is the same

for a consumers and producers, from equation 1, 2 & 3

MRSxy of A = MRSxy of B = MRTxy

Thus, perfect competition satisfies the marginal condition required for the pareto optimal.

Second Fundamental Theorem

The second fundamental theorem says that each Pareto optimum can be achieved via a competitive equilibrium, if lump-sum taxes and transfers are available to shift individual endowments.

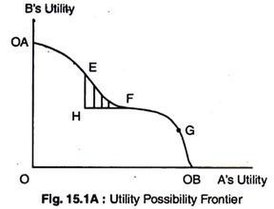

the utility possibility curve

In welfare economics, a utility–possibility frontier (or utility possibilities curve), is a widely used concept analogous to the better-known production–possibility frontier. The graph shows the maximum amount of one person’s utility given each level of utility attained by all others in society.

The Social Welfare Function

The second theorem states that any Pareto optimum can be supported as a competitive equilibrium for some initial set of endowments. The implication is that any desired Pareto optimal outcome can be supported; Pareto efficiency can be achieved with any redistribution of initial wealth.

Maximum Social Welfare

Social welfare is maximized (a ‘fair’ distribution of utility) when the utility possibilities curve is tangent to the highest attainable utility indifference curve. If necessary to ensure fairness, the government should redistribute income, but then step out of the way – no interference with prices or allocation.

Pareto Optimality & imperfect Competition Market

The Pareto optimally has been supported by perfect competition as a market structure where efficiency is sustainable, but it is imperfect competition where there are higher increasing returns and better redistribution, through innovation and growth, promoted by the market size.