unit 3

Interest Rates

Meaning of Interest rate

The interest rate is the amount charged on top of the principal by a lender to a borrower for the use of assets for the specified period of time. It is a percentage term.

Simple Interest Rate = Principal × Interest Rate × Time.

Compound Interest = Principal × [(1 + Interest Rate)n −1]

APR (Annual Percentage Rate)

The Annual Percentage Rate (APR) is the cost you pay each year to borrow money, including fees, expressed as a percentage. The APR is a broader measure of the cost to you of borrowing money since it reflects not only the interest rate but also the fees that you have to pay to get the loan.

APY (Annual Percentage Yield)

APY is calculated using this formula: APY= (1 + r/n )n – 1, where “r” is the stated annual interest rate and “n” is the number of compounding periods each year. APY is also sometimes called the effective annual rate, or EAR.

Determination of Interest Rate

Here we are going to discuss the theories of determination of rate of interest. They are:

- Classical Theory

- Loanable Funds Theory

- Theory of Liquidity Preference

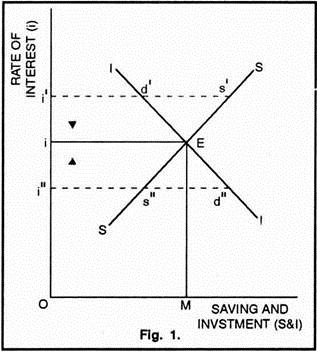

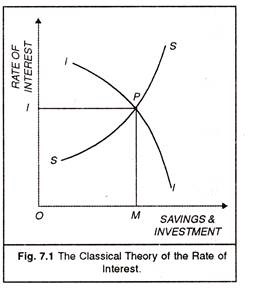

1.Classical Theory

According to the classical theory, the rate of interest rate is determined by the intersection of. demand for and supply of investment (or capital). Interest is the price of investment because. firms borrow money for investment. Thus, investment depends on interest rate

Demand for Investment

According to the classical theory, the demand for capital comes only from the investors for meeting investment expenditures. It completely ignores the fact that loans are also taken for consumption purposes.

Supply of Savings

Saving means curtailment of consumption or postponement of the present consumption. Thus, saving involves a sacrifice, abstinence or waiting. The rate of interest is considered to be the reward for abstinence or waiting. It is an inducement for the act of saving or foregoing the present consumption.

Equilibrium Rate of Interest in the Classical Theory

In the classical theory the equilibrium rate of interest is the one which equals the supply of loanable funds to the demand for loanable funds .

Criticism of Classical Theory of Interest

1. Based on the Assumption of Full Employment:

2. Ignores Effect of Changes in Income Level

3. Wrongly Assumes Independence of Saving and Investment Demand Schedules

4. Savings out of Current Income not the only Source of Loanable Funds

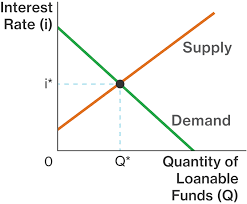

2. Loanable Funds Theory

In economics, the loanable funds doctrine is a theory of the market interest rate. According to this approach, the interest rate is determined by the demand for and supply of loanable funds. The term loanable funds includes all forms of credit, such as loans, bonds, or savings deposits.

Demand for Loanable Funds: (LD)

A hypothetical curve that shows the willingness to borrow money to fund investment projects; as the interest rate decreases, the quantity of loans demanded will increase.

Demand for Loanable Funds

Investment (I):The main source of demand for loanable funds is the demand for investment. Investment refers to the expenditure for the purchase of making of new capital goods including inventories. The price of obtaining such funds for the purpose of these investments depends on the rate of interest.

Hoarding (H):The demand for loanable funds is also made up by those people who want to hoard it as idle cash balances to satisfy their desire for liquidity. The demand for loanable funds for hoarding purpose is a decreasing function of the rate of interest. At low rate of interest demand for loanable funds for hoarding will be more and vice-versa

Dissaving (DS):Dissaving’s is opposite to an act of savings. This demand comes from the people at that time when they want to spend beyond their current income. Like hoarding it is also a decreasing function of interest rate.

Supply of Loanable Funds: (LS)

The supply of loanable funds represents the behavior of all of the savers in an economy. The higher interest rate that a saver can earn, the more likely they are to save money. As such, the supply of loanable funds shows that the quantity of savings available will increase as the interest rate increases.

- Savings (S):

Savings constitute the most important source of the supply of loanable funds. Savings is the difference between the income and expenditure. Since, income is assumed to remain unchanged, so the amount of savings varies with the rate of interest. Individuals as well as business firms will save more at a higher rate of interest and vice-versa. - Dishoarding (DH):

Dishoarding is another important source of the supply of loanable funds. Generally, individuals may dishoard money from the past hoardings at a higher rate of interest. Thus, at a higher interest rate, idle cash balances of the past become the active balances at present and become available for investment. If the rate of interest is low dishoarding would be negligible. - Disinvestment (DI):

Disinvestment occurs when the existing stock of capital is allowed to wear out without being replaced by new capital equipment. Disinvestment will be high when the present interest rate provides better returns in comparison to present earnings. Thus, high rate of interest leads to higher disinvestment and so on. - Bank Money (BM):

Banking system constitutes another source of the supply of loanable funds. The banks advance loans to the businessmen through the process of credit creation. The money created by the banks adds to the supply of loanable funds.

Determination of Rate of Interest in Loanable Funds Theory

According to loanable funds theory, equilibrium rate of interest is that which brings equality between the demand for and supply of loanable funds. In other words, equilibrium interest rate is determined at a point where the demand for loanable funds curve intersects the supply curve of loanable funds.

Criticism of Loanable Funds Theory

The loanable funds theory has been criticised for combining monetary factors with real factors. It is not correct to combine real factors like saving and investment with monetary factors like bank credit and dishoarding without bringing in changes in the level of income. This makes the theory unrealistic.

Improvement over the Classical Theory

Loanable funds theory is considered to be an improvement over the classical theory on the following aspects:

1.Loanable funds theory recognizes the importance of hoarding as a factor affecting the interest rate which the classical theory has completely overlooked.

- Loanable funds theory links together liquidity preference, quantity of money, savings and investment.

- Loanable funds theory takes into consideration the role of bank credit which acts as a very important source of loanable funds.

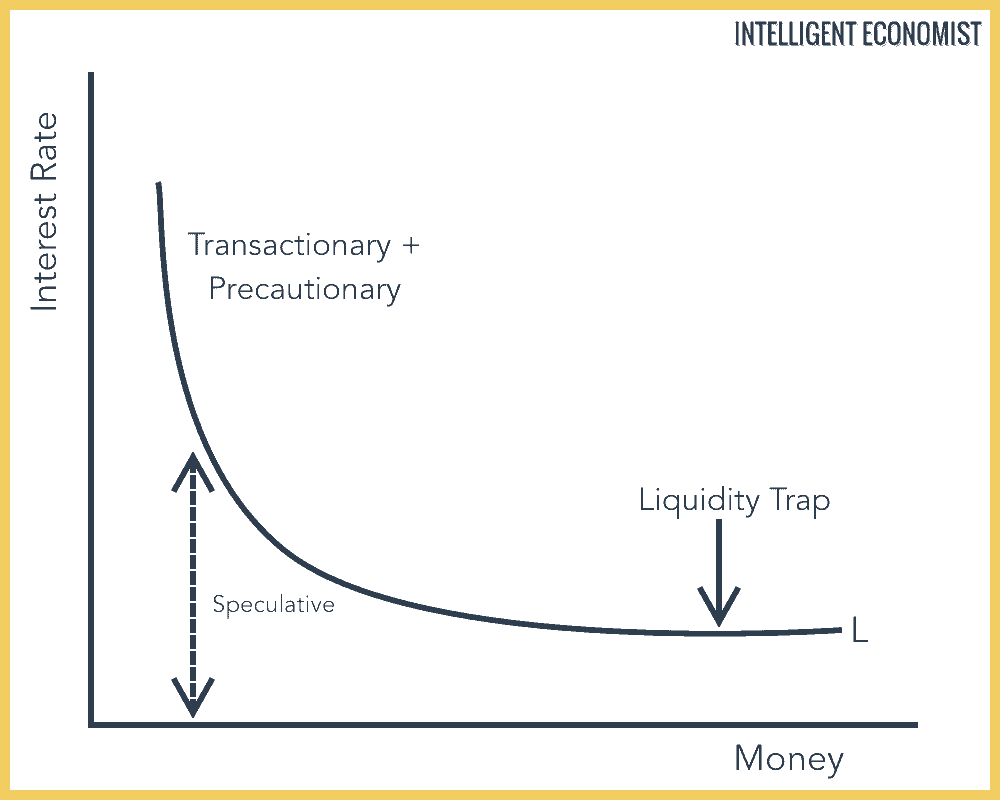

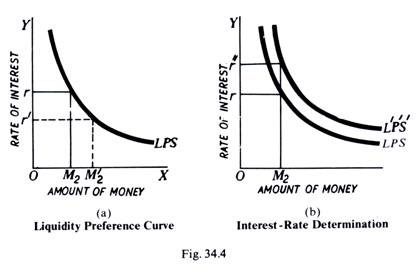

theory of liquidity preference

Liquidity Preference Theory is a model that suggests that an investor should demand a higher interest rate or premium on securities with long-term maturities that carry greater risk because, all other factors being equal, investors prefer cash or other highly liquid holdings.

Demand for Money:

Demand for money is not to be confused with the demand for a commodity that people ‘consume’. But since money is not consumed, the demand for money is a demand to hold an asset. The desire for liquidity or demand for money arises because of three motives:

(a) Transaction motive

(b) Precautionary motive

(c) Speculative motive

Determination of Interest Rate as per Liquidity Preference Theory:

John Maynard Keynes’ liquidity preference theory concentrates on the demand and supply for money as the interest rate determinants. According to his proposition that interest rate is the price paid for borrowed money, people will rather keep cash with themselves than invest cash in assets.

Limitations of the theory of Liquidity Preference

One of the biggest limitations of the liquidity preference theory is that it assumes that the employment rate is constant. In reality, the employment rate is not constant, and it is constantly changing. The second criticism is that this theory assumes a certain level of income.

Sources of Interest Rate Differentials

7 Main Causes of Difference in Interest Rate

- Cause # 1. Differences in Risk:

- Cause # 2. Period of Loan:

- Cause # 3. Volume of Loan:

- Cause # 4. Nature of Security:

- Cause # 5. Financial Standing of the Borrower:

- Cause # 6. Market Imperfection:

- Cause # 7. Variation in Demand and Supply of Money