Unit 4

Banking System

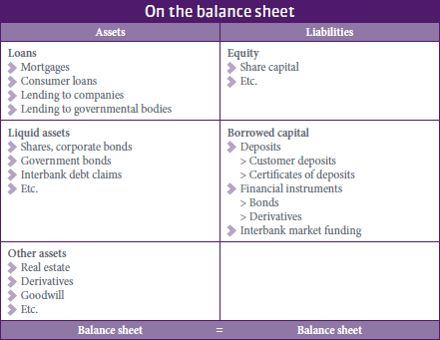

Balance Sheet of Commercial Bank

The balance sheet of a commercial bank is a statement of its liabilities and assets at a particular point of time. Liabilities refers to all debit item representing the obligations of all the bank or others claims of the bank.

Portfolio Management of a Commercial Bank

Portfolio management by banks is the process of effectively and prudently managing mix of assets and liabilities. In this process banks acquire and dispose of its assets meant for earning income. A large percentage of bank’s funds contain deposits in different type of accounts both demand and term deposits.

Objectives of Portfolio Management:

There are three main objectives of portfolio management which a wise bank follows: liquidity, safety and income. The three objectives are opposed to each other. To achieve on the bank will have to sacrifice the other objectives.

Theories of Portfolio Management:

The theory of portfolio management describes the resulting risk and return of a combination of individual assets. A primary objective of the theory is to identify asset combinations that are efficient. Here, efficiency means the highest expected rate of return on an investment for a specific level of risk.

The Real Bills Doctrine

According to the real bills doctrine, limiting banks to only or primarily issuing money that is adequately backed by equally valued assets will not contribute to inflation. By contrast, proponents of quantity theory argue that any increases in the money supply tend to create inflation

The Shiftability Theory

In banking, shiftability is an approach to keep banks liquid by supporting the shifting of assets. When a bank is short of ready money, it is able to sell or repo its assets to a more liquid bank.

The Anticipated Income Theory

This theory states that irrespective of the nature and feature of a borrower’s business, the bank plans the liquidation of the term-loan from the expected income of the borrower. A term-loan is for a period exceeding one year and extending to a period less than five years.

The Liabilities Management Theory

This theory states that, there is no need for banks to lend self-liquidating loans and maintain liquid assets as they can borrow reserve money in the money market whenever necessary. A bank can hold reserves by building additional liabilities against itself via different sources.

Indian Banking System

Changing Role and Structure of Indian Banking System

Banks in India have now become very customer and service focus. Their service has become quick, efficient and customer-friendly. This positive change is mostly due to rising competition from new private banks and initiation of Ombudsman Scheme by RBI.

The following points briefly highlight the changing role of banks in India.

- Better customer service,

- Mobile banking facility,

- Bank on wheels scheme,

- Portfolio management,

- Issue of electro-magnetic cards,

- Universal banking,

- Automated teller machine (ATM), .

- Internet banking,

- Encouragement to bank amalgamation,

- Encouragement to personal loans, .

- Marketing of mutual funds,

- Social banking, etc.

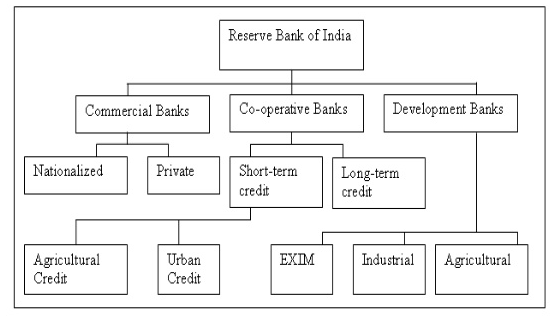

Structure of Indian Banking System

The structure of the banking system of India can be broadly divided into scheduled banks, non-scheduled banks and development banks. Banks that are included in the second schedule of the Reserve Bank of India Act, 1934 are considered to be scheduled banks.

Banking Sector Reforms in India

The banking sector is the heart of all the economic activity of a country and a small change in its regulation affects the entire economy. The banks are the institutions that impinge on the economy and affect their performance for better or worse. The banking system helps in

• Capital accumulation • Growth by encouraging savings • Mobilising the capital • Allocating the capital for alternative uses, etc.

History of Banking Sector Reforms in India

By the 1960s, the banking sector was contributing a good share to the Indian economy. It became important to regulate and control to maintain the balance in the economy. This led to the introduction of the Nationalization of Banks Act 1964. This act led to the nationalization of 14 major commercial banks in India.

Reasons behind the Banking Reforms in India

Importance of Banking Sector Reforms and ActsIt is to promote healthy competition for better productivity. Foreign direct investment is another area they focus on to improve the economy. The merging of banks across India is their focus again. It is done to improve efficiency and productivity.

What are the reasons behind banking sector reforms in India?

Objectives of Banking Sector Reforms in India

The main objective is to improve operational efficiency and promote banks’ health and financial reliability, so that Indian banks can meet internationally recognised standards of performance.

- Current Scenario. …

- Banking Reforms. …

- Road Ahead.